Beyond Competitive Benchmarking: A Systematic Approach to Cost Reduction in Robotics Manufacturing

How cross-industry technology transfer achieves 25-40% cost reductions where traditional benchmarking plateaus at 5-10%. A technical framework for robotics manufacturers.

The Global Context: Supply Chain Diversification

The robotics industry is experiencing a fundamental restructuring of its supply chain. Historically concentrated in Japan, Germany, and the United States, component manufacturing has globalized significantly over the past decade.

Key Drivers:

Patent cliff effects: Critical patents from the 1990s-2000s entering public domain

Technology maturation: Manufacturing processes becoming standardized

Market demand: Humanoid robotics creating massive scale requirements

Geopolitical factors: Supply chain resilience prioritization

This article examines cost reduction strategies applicable globally, with case studies drawn from manufacturers across multiple regions. The principles of cross-industry technology transfer apply regardless of a company’s location or supply chain structure.

Introduction: The Cost Reduction Paradox

In the global robotics industry, “competitive benchmarking” has become the default playbook for cost reduction. Engineering teams worldwide follow a familiar ritual: disassemble competitors’ products, analyze their components, reverse-engineer their solutions, and attempt to replicate their cost structures.

Yet this widespread practice has led to an unexpected outcome: the more companies benchmark their competitors, the harder it becomes to achieve breakthrough cost reductions.

This article explores why competitive benchmarking alone is insufficient and presents a systematic framework for cost optimization through cross-industry technology transfer—a methodology that has helped manufacturers achieve 25-40% cost reductions where traditional approaches plateau at 5-10%.

Part I: Understanding the Cost Landscape Across Robot Types

The robotics industry encompasses diverse product categories, each with distinct cost structures requiring tailored optimization strategies.

1.1 Industrial Robots: The Global Component Market Evolution

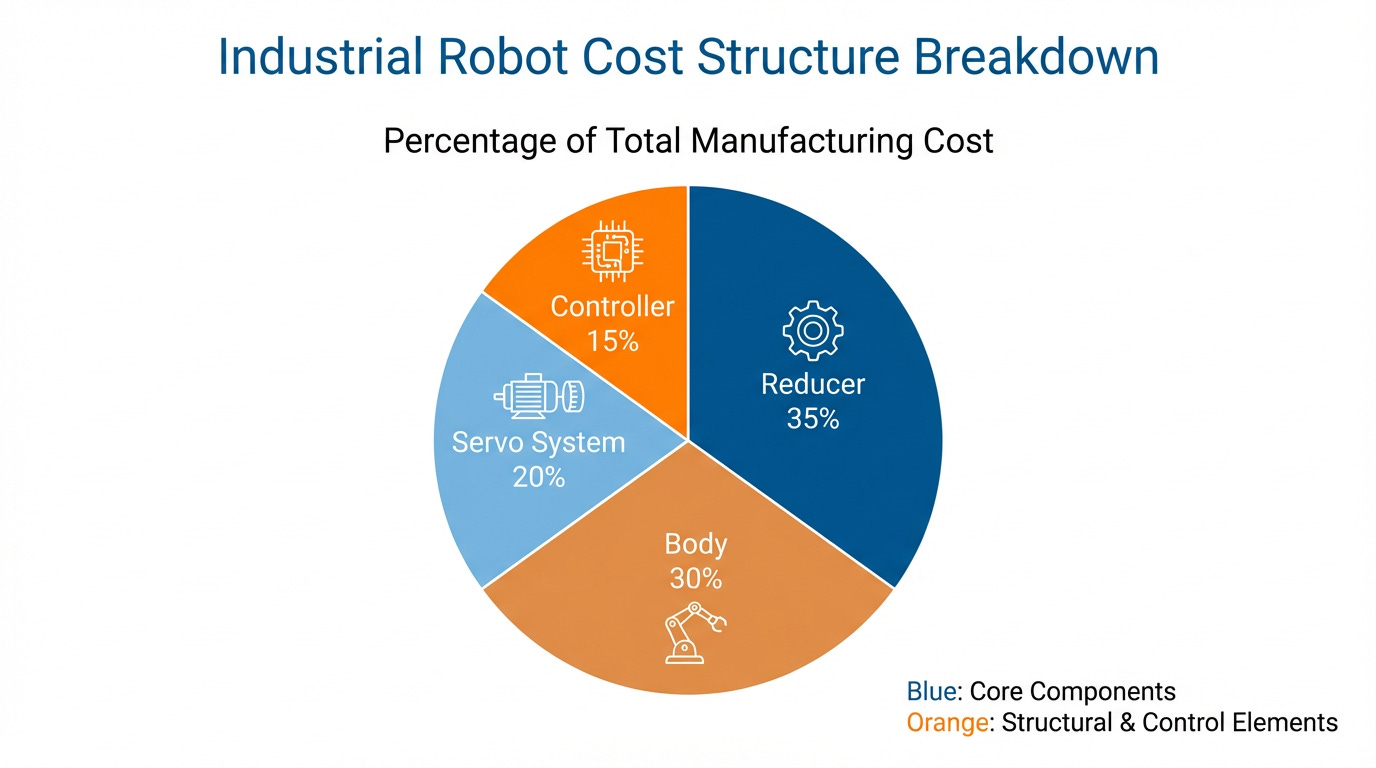

Figure 1: Cost breakdown of industrial robots showing the concentration of value in core components

Cost Structure:

Reducers: 35% (Harmonic drives: $3,000-$8,000 per unit)

Servo Systems: 20%

Controllers: 15%

Body & Assembly: 30%

Core components account for over 70% of total manufacturing costs. This concentration makes component-level innovation critical for any manufacturer, regardless of location.

Case Study: Precision Reducer Market Transformation

The precision reducer market illustrates how technology maturation drives global cost reduction:

Historical Market Structure (pre-2018):

Dominated by Japanese manufacturers (75%+ global market share)

High barriers to entry (precision manufacturing, IP protection)

Limited price competition

Average cost: $8,000-$12,000 per unit

Current Market Dynamics (2025):

Multiple qualified suppliers across regions

Performance parity achieved by new entrants

Competitive pricing pressure

Average cost: $3,000-$6,000 per unit

Technical Achievements by New Entrants:

Precision lifespan: 200 million cycles (exceeding established standards)

Size reduction: 40% volume decrease

Manufacturing scalability: Annual production capacity >1 million units

Global supply chain integration: Supporting major OEMs worldwide including Tesla, ABB, and FANUC

Impact on Robotics Manufacturers:

This supply chain diversification benefits the entire industry:

✓ Reduced component costs

✓ Improved supplier negotiating position

✓ Faster innovation cycles

✓ Supply chain resilience

✓ Geographic optionality

Key Insight: Technology democratization, not geography, drives cost reduction. Manufacturers in North America, Europe, and Asia all benefit from competitive supplier ecosystems.

Body Structure Innovation: Global Best Practices

Multiple manufacturers worldwide have demonstrated lightweighting potential through advanced manufacturing techniques:

Example: Modern Manufacturing Approaches

Full cast-aluminum construction

30% weight reduction vs. welded alternatives

Integrated component routing

Enhanced structural rigidity

Technology Sources:

Automotive die-casting (Tesla, Toyota, BMW)

Aerospace composite structures (Boeing, Airbus)

Consumer electronics unibody design (Apple, Samsung)

Implementation Results:

Material cost reduction: 15-20%

Assembly time savings: 40%

Quality consistency improvement: 35%

Reduced tooling complexity

These techniques are geography-agnostic and transferable across regions, with successful implementations documented in North American, European, and Asian manufacturing facilities.

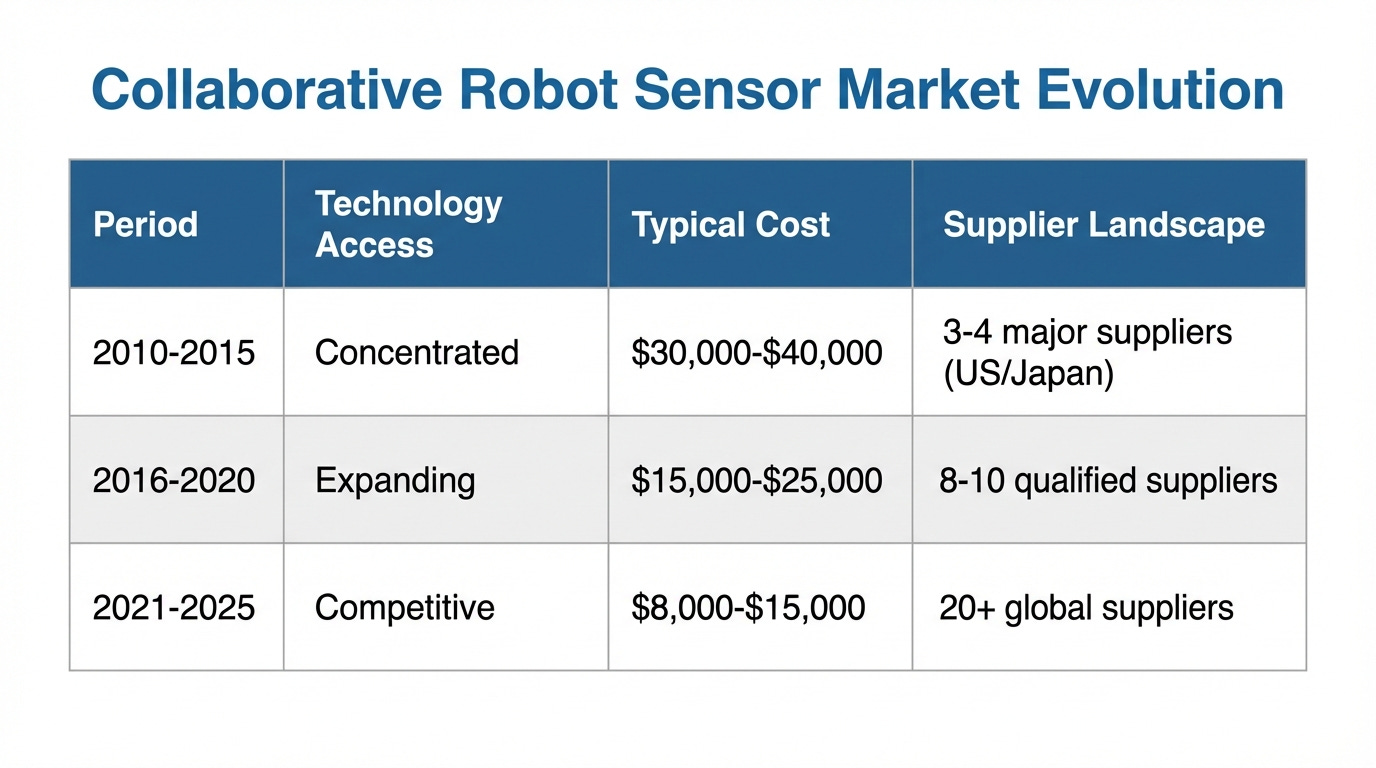

1.2 Collaborative Robots: Global Sensor Market Maturation

Collaborative robots (cobots) face unique cost pressures from safety requirements, but the component landscape has evolved dramatically.

The Safety Sensor Economics:

Force/torque sensing represents a significant cost driver in collaborative robotics. The market has evolved from a concentrated oligopoly to a competitive global ecosystem.

Market Evolution Timeline:

Drivers of Cost Reduction:

Technology maturation: Manufacturing processes standardized

Patent expirations: Core IP entering public domain

Volume production: Humanoid robotics driving scale

Regional production: Manufacturing closer to end markets

Alternative technologies: Current-based sensing reducing sensor dependency

Geographic Distribution of Qualified Suppliers (2025):

North America: 6 suppliers

Europe: 5 suppliers

Asia: 12 suppliers

Other regions: 2 suppliers

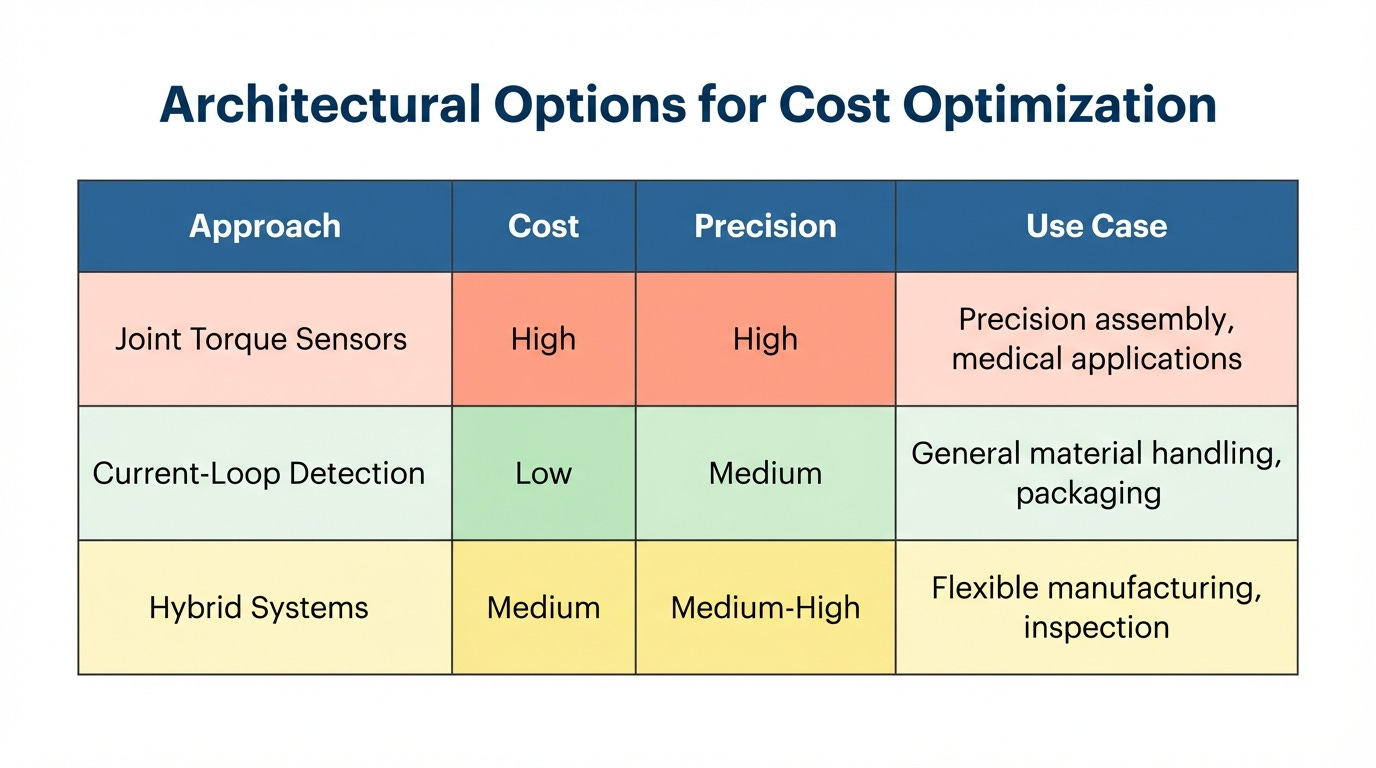

Architectural Options for Cost Optimization:

Strategic Implications:

Modern cobot manufacturers can:

Source from multiple qualified suppliers globally

Negotiate competitive pricing

Maintain supply chain resilience

Choose optimal cost-performance balance

This represents industry maturation, not regional dominance—quality sensors are available worldwide at dramatically reduced costs compared to a decade ago.

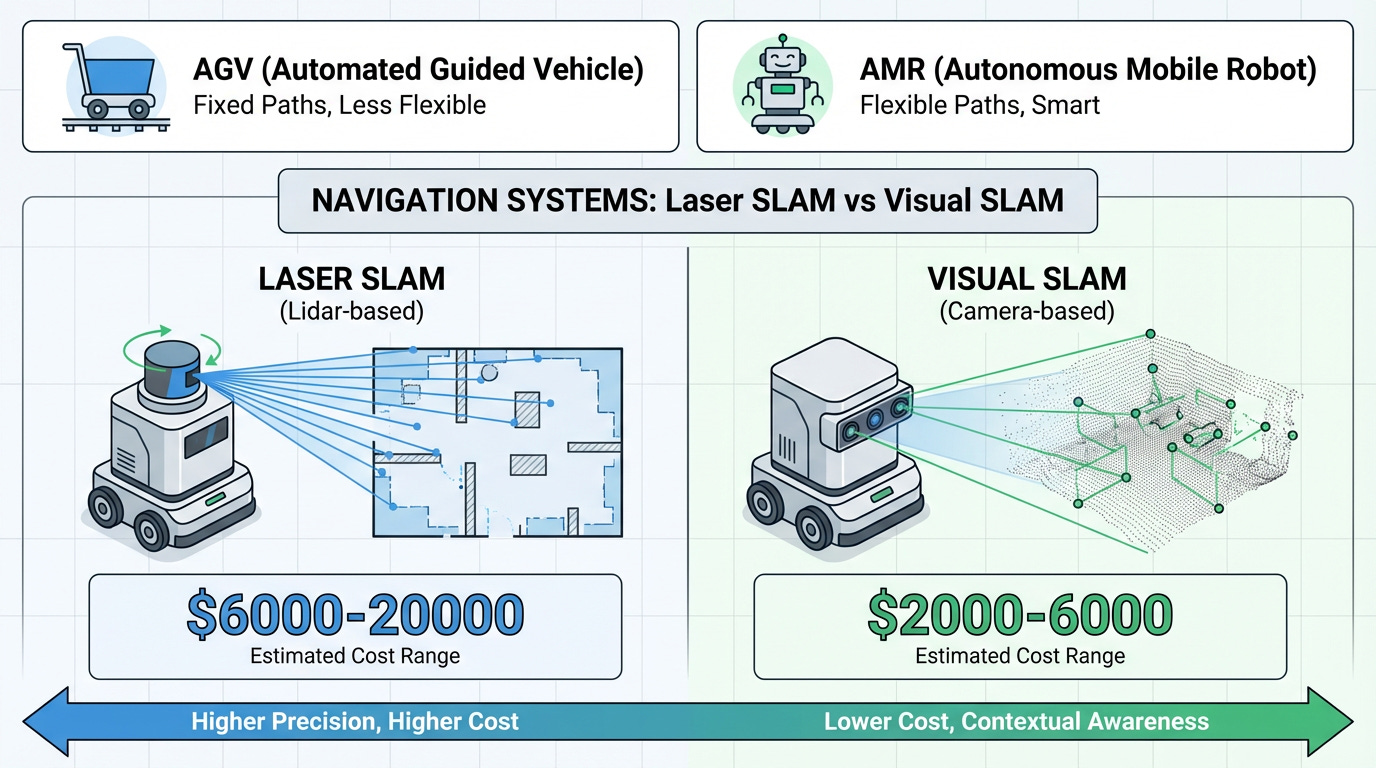

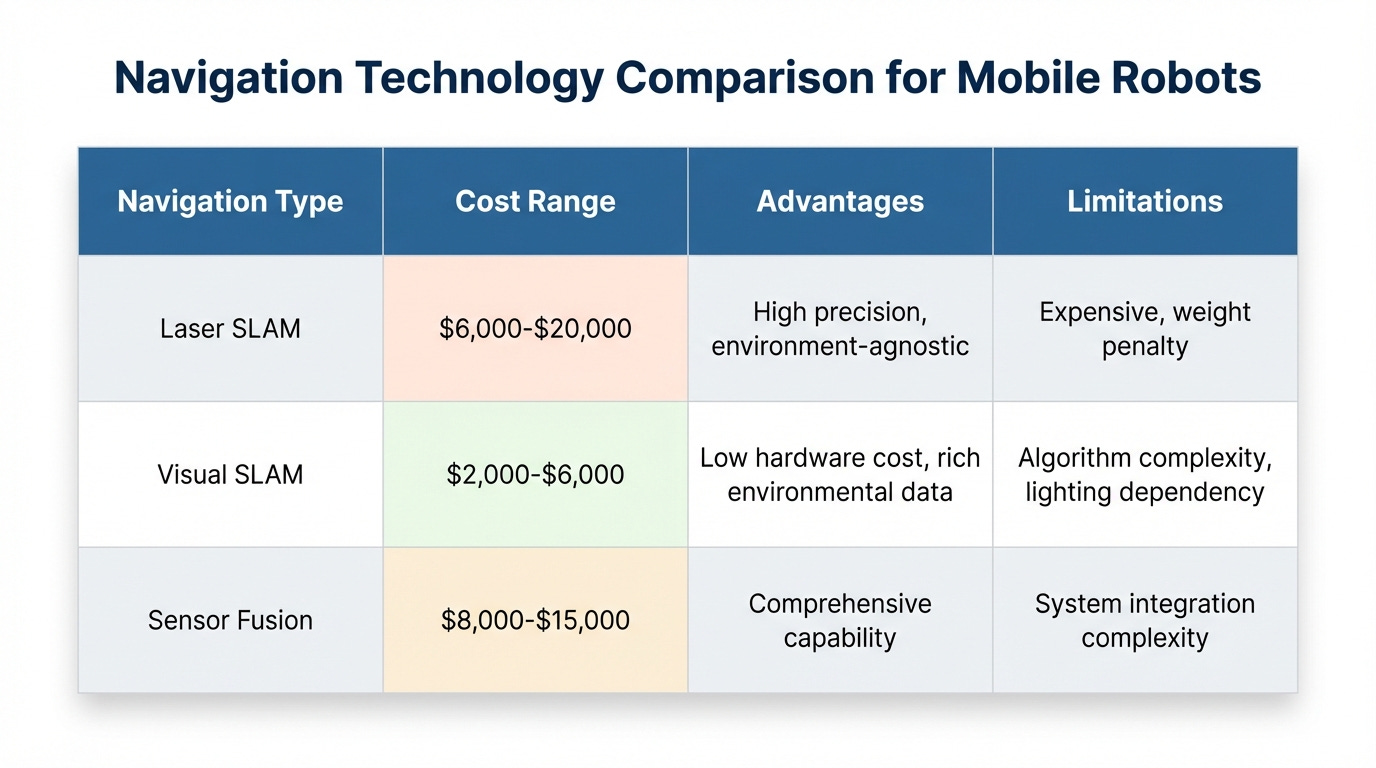

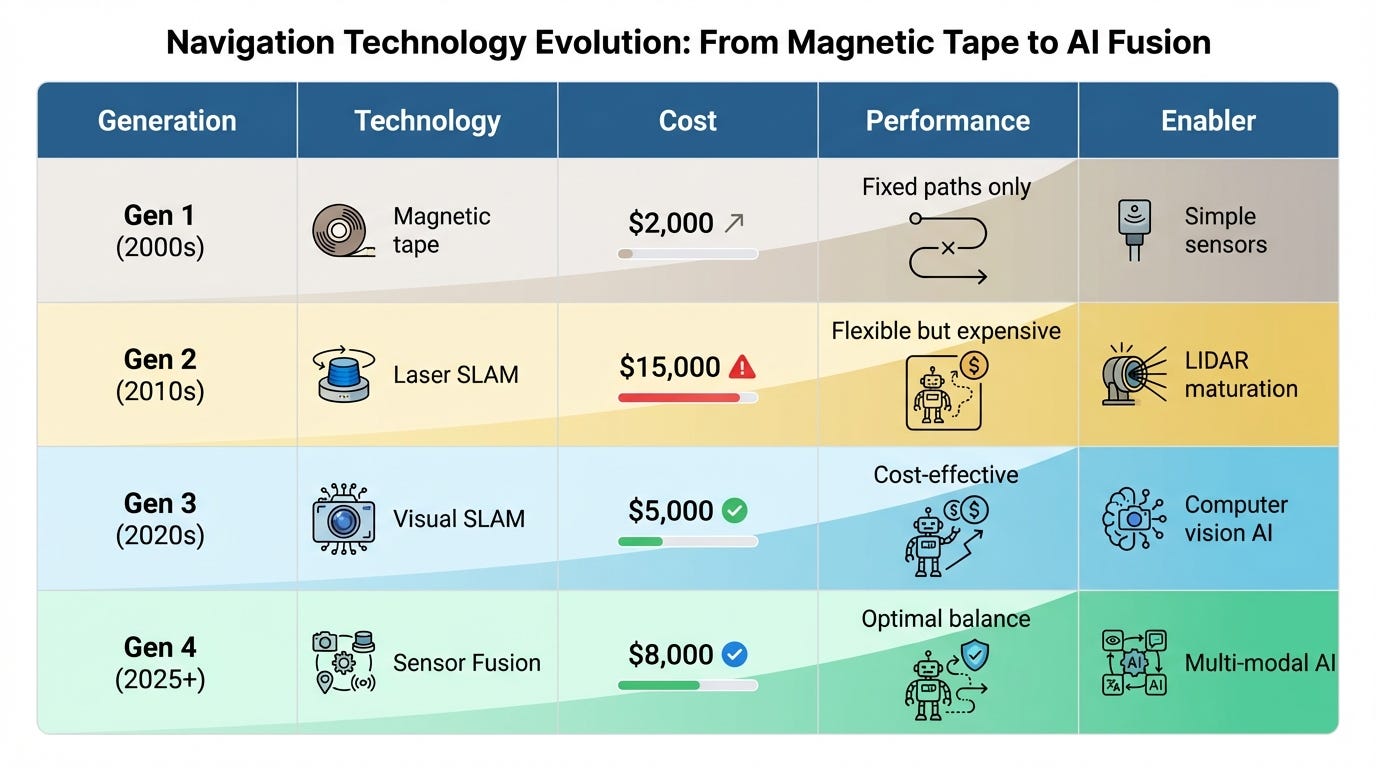

1.3 Mobile Robots (AMR/AGV): The Navigation Economics

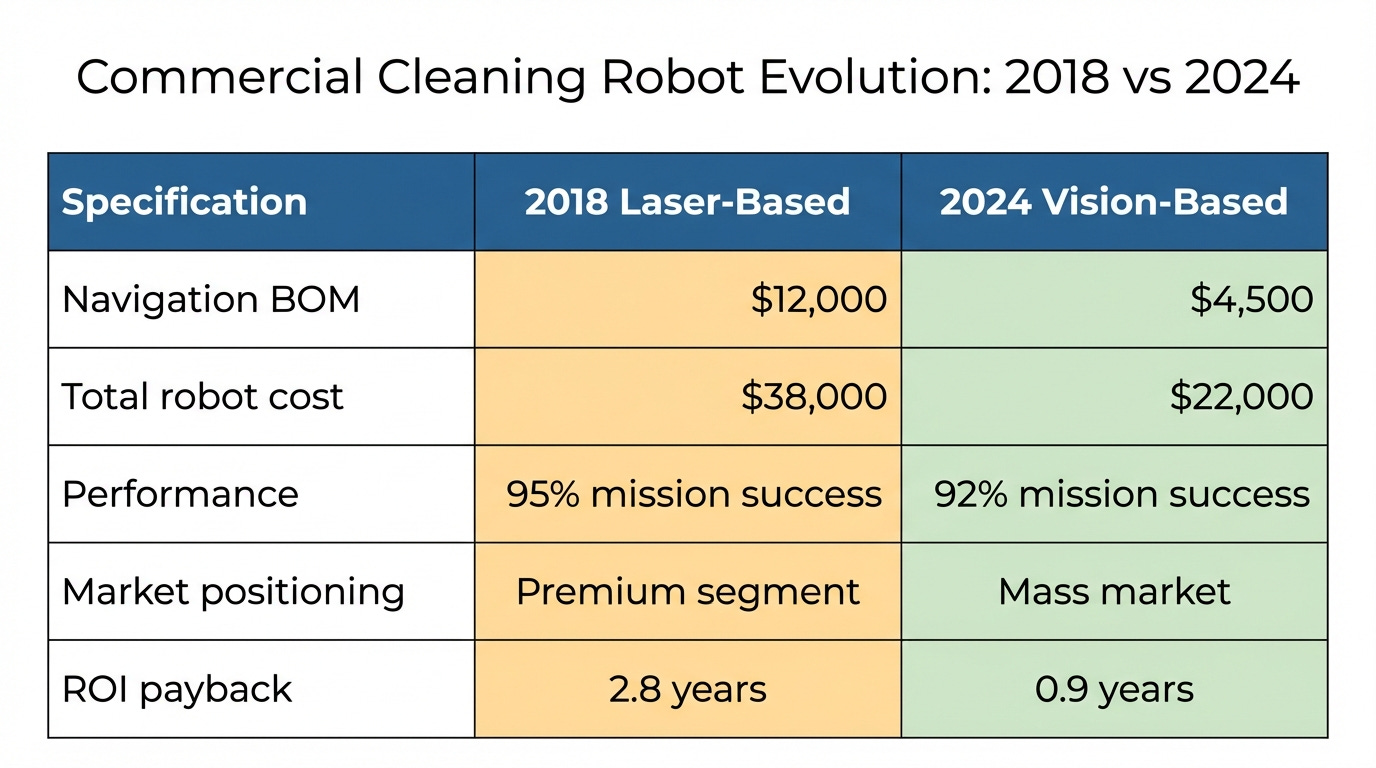

Figure 2: Comparative analysis of laser SLAM vs visual SLAM navigation systems showing the dramatic cost differential

Navigation systems represent 40% of mobile robot costs, creating a critical optimization opportunity.

Technology Comparison:

Technology Evolution Drivers:

The dramatic cost reduction in visual navigation stems from:

Autonomous vehicle R&D spillover: Billions invested in computer vision

Embedded computing advances: High-performance SoCs at consumer price points

Algorithm maturation: Open-source SLAM frameworks (ORB-SLAM, RTAB-Map)

Component commoditization: Industrial-grade cameras <$200

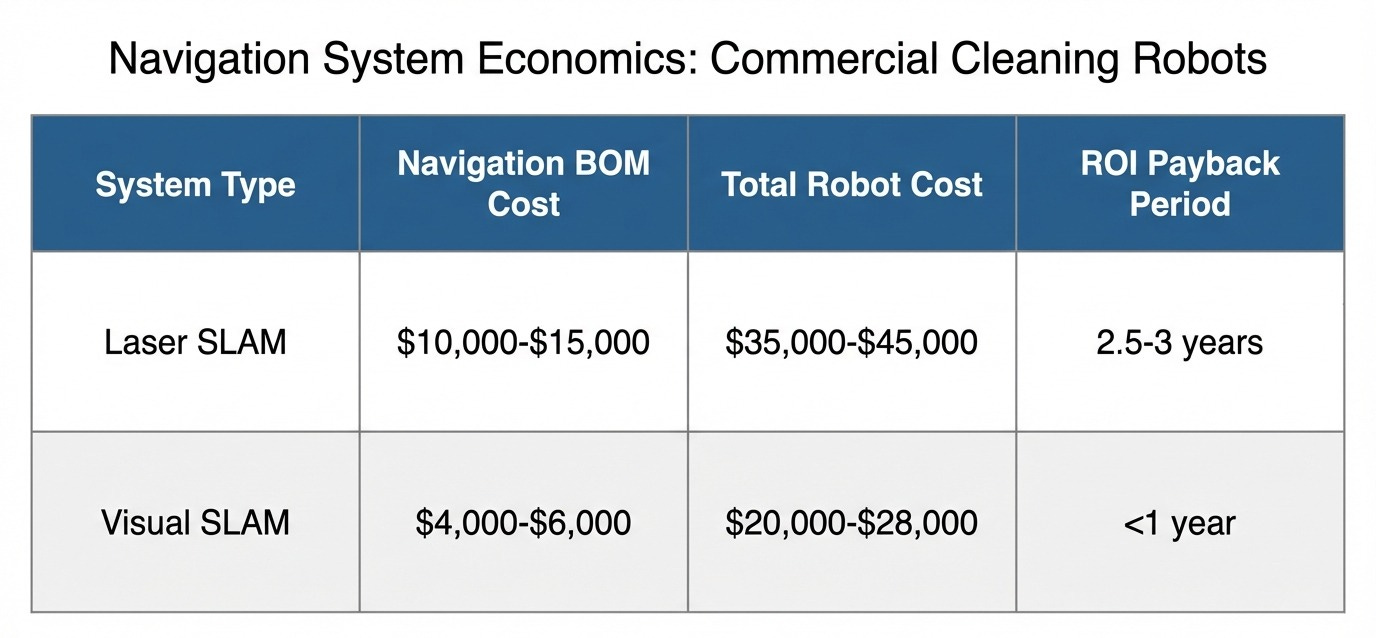

Market Impact Analysis:

Commercial cleaning robots exemplify the economics:

This cost structure transformation has:

Unlocked mass market adoption in hospitality and retail

Enabled ROI-positive deployments in mid-size facilities

Accelerated market penetration in price-sensitive segments

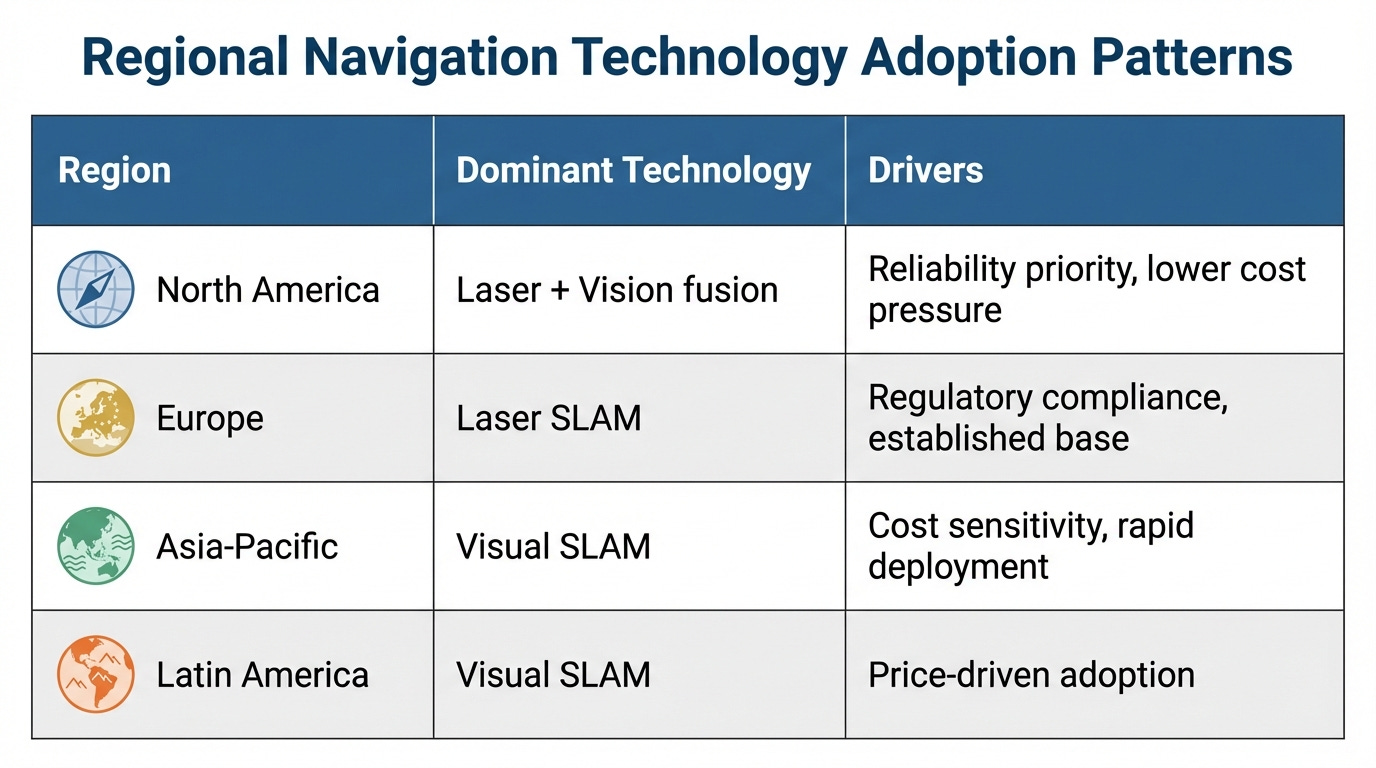

Regional Deployment Patterns:

Interestingly, technology choice varies by market maturity:

Mature markets (US, EU, Japan): Hybrid systems gaining share

Emerging markets (Southeast Asia, Latin America): Visual SLAM dominance

Industrial environments globally: Laser SLAM remains standard for mission-critical applications

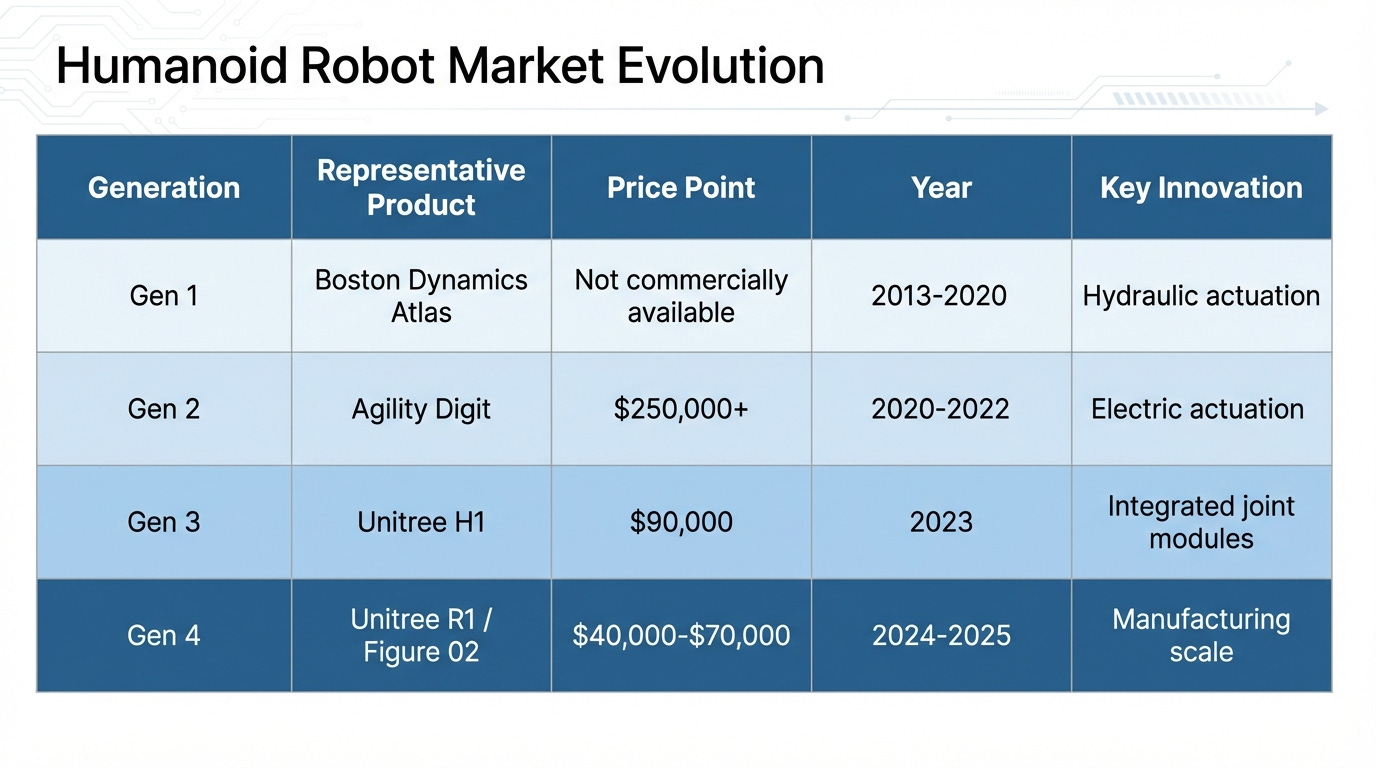

1.4 Humanoid & Quadruped Robots: The Scaling Challenge

Humanoid robots represent the frontier of cost reduction innovation, with dramatic price compression over the past 24 months.

Cost Structure:

Joint modules: ~30%

Perception systems: 15-20%

Computing platforms: 10-15%

Body structure: 20-25%

Integration & assembly: 10-15%

Market Price Evolution:

Breakthrough Pricing: Sub-$50K Humanoids

Recent announcements demonstrate rapid cost reduction:

Unitree R1: $39,900 (consumer-grade specifications)

Figure 02: $60,000-$70,000 (industrial-grade, BMW deployment)

Tesla Optimus: Projected $20,000-$30,000 at scale (2026+ estimate)

Key Success Factors Enabling Cost Reduction:

Technology Reuse from Quadruped Platforms

Proven joint designs

Validated control algorithms

Mature supply chains

Reduced R&D amortization

Manufacturing Scale Economics

Volume commitments enabling supplier investment

Automated assembly lines

Standardized testing protocols

Shared tooling across product families

Design-for-Manufacturing Principles

Part count reduction: 40% fewer components vs. Gen 2

Assembly time optimization: <2 hours total assembly

Standard fasteners and connectors throughout

Modular serviceability

Vertical Integration of Critical Components

In-house joint module production

Custom ASIC development for control

Proprietary battery systems

Integrated manufacturing eliminates supplier margins

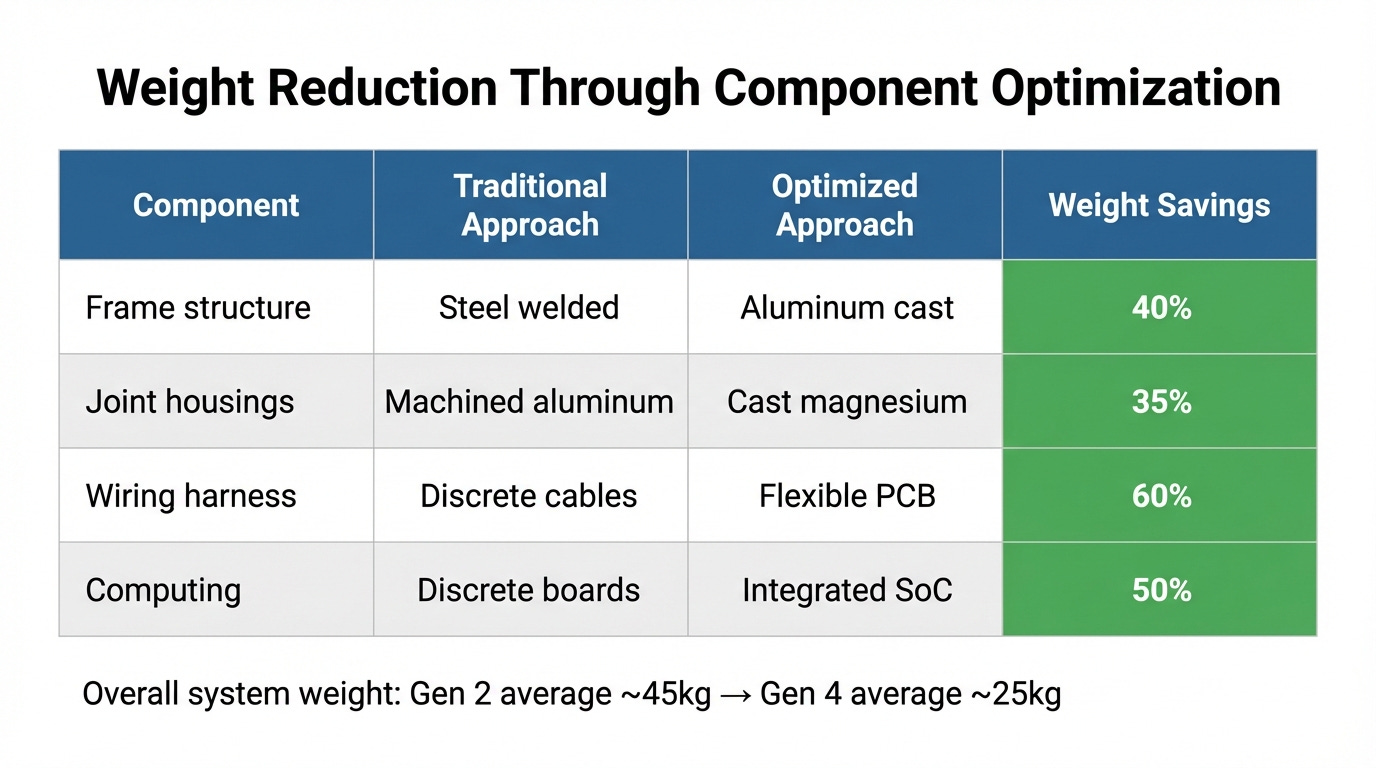

Weight Reduction Achievements:

Manufacturing Maturity Indicators:

The humanoid sector is transitioning from R&D to manufacturing:

Production volumes: Single units → Hundreds per month

Supply chain: Custom one-offs → Standard catalog parts

Quality systems: Lab validation → ISO 9001/IATF 16949

Service infrastructure: Factory-only → Distributed service centers

Part II: The Structural Limitations of Competitive Benchmarking

2.1 The Follower’s Dilemma

Competitive benchmarking suffers from an inherent asymmetry: you see your competitor’s solution, but not their problem-solving process.

When you reverse-engineer a competitor’s product, you observe:

✓ Component selection

✓ Assembly methods

✓ Material choices

✓ Final specifications

But you don’t see:

✗ Failed prototypes and design iterations

✗ Constraint trade-offs during development

✗ Patent landscapes navigated

✗ Supplier capability limitations encountered

✗ Cost-benefit analyses that drove decisions

This information asymmetry ensures you remain perpetually one step behind.

Real-World Example:

A North American robotics manufacturer spent 14 months reverse-engineering a competitor’s innovative gripper mechanism, successfully replicating its functionality. However:

Development cost: $480,000

Performance: 92% of original (subtle material science differences)

Market entry: 18 months after competitor

Patent issues: Required $120,000 redesign to avoid infringement

Outcome: Total investment of $600,000 to achieve parity with 18-month lag—resources that could have funded original innovation.

2.2 The Patent Maze

Mature products are protected by extensive IP portfolios. Attempting to replicate designs leads to complex navigation challenges.

Patent Avoidance Costs:

Increased redesign complexity

Performance compromises to avoid infringement

Extended development timelines

Higher engineering resource consumption

Legal consultation expenses

Case Study: Precision Bearing System

A European manufacturer attempted to replicate a patented crossed-roller bearing arrangement used in competitive robotic joints:

Timeline:

Month 0-6: Initial reverse engineering and design replication

Month 7: Patent infringement identified during legal review

Month 8-18: Alternative design development (”design-around”)

Month 19-24: Testing and validation of modified design

Results:

Engineering cost: 40% higher than original estimate

Performance: 15% lower load capacity

Patent freedom: Achieved, but at significant cost

Time-to-market: 18-month delay

Alternative Approach:

Cross-industry technology transfer from aerospace bearing applications could have yielded:

Patent-free design inspiration

Potentially superior performance

Faster development cycle

Differentiated market positioning

2.3 Cognitive Lock-In

The most insidious limitation is cognitive: when all your references come from the same industry, your solution space contracts.

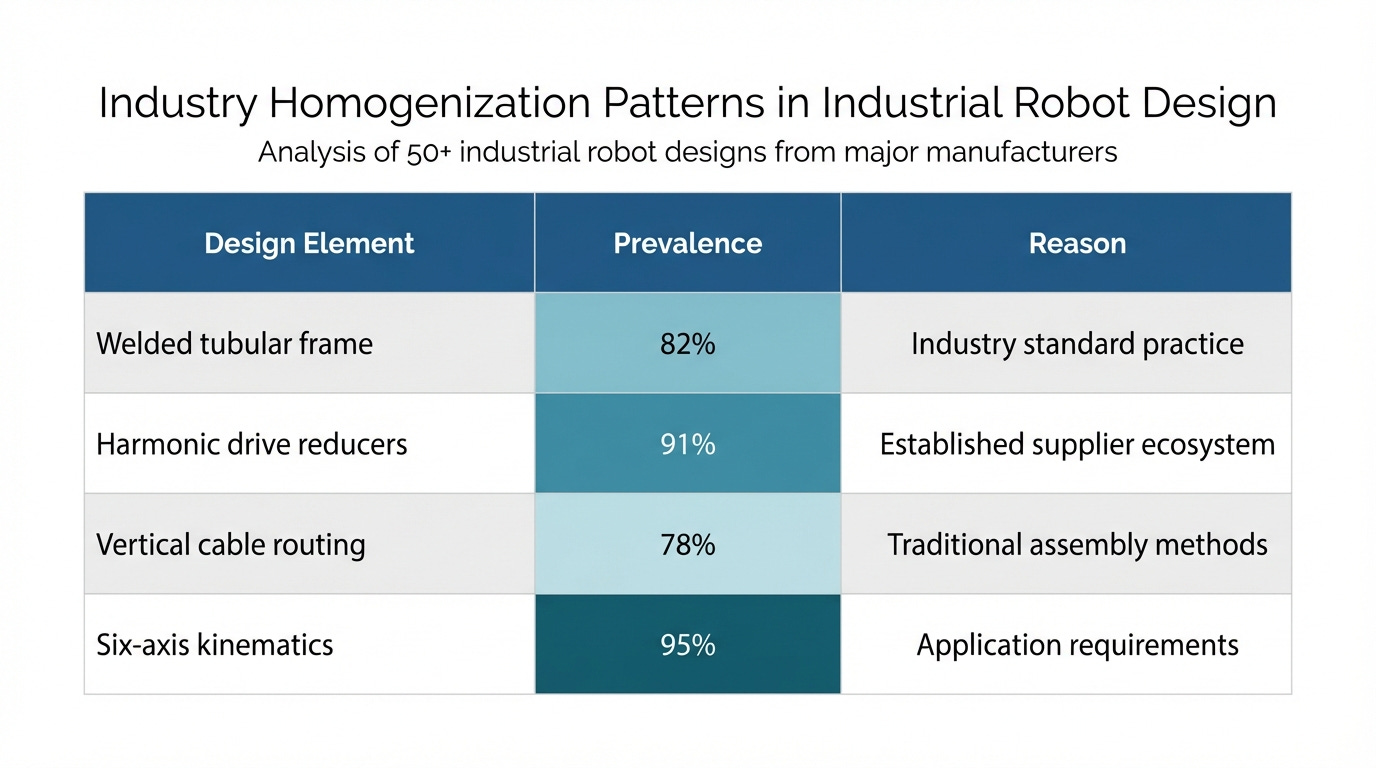

Industry Homogenization Patterns:

Convergent Evolution Problem:

When all engineers study the same references:

Design languages converge

Innovation becomes incremental

Cost optimization hits plateau

Differentiation becomes superficial

Example: Frame Construction

From 2010-2020, virtually all collaborative robot manufacturers used welded tubular steel frames because:

“Industry best practice”

Existing supplier relationships

Familiar to engineering teams

“Proven” technology

Result: Cost improvement of only 8% over decade through process optimization.

Paradigm Shift (2020+):

Manufacturers examining automotive and aerospace manufacturing adopted:

Investment casting (40% part count reduction)

Aluminum extrusion assemblies (35% weight reduction)

Composite structures (specialized applications)

New results: 25-35% cost reduction + performance improvements.

The lesson: Industry conventions often represent local optima, not global optima.

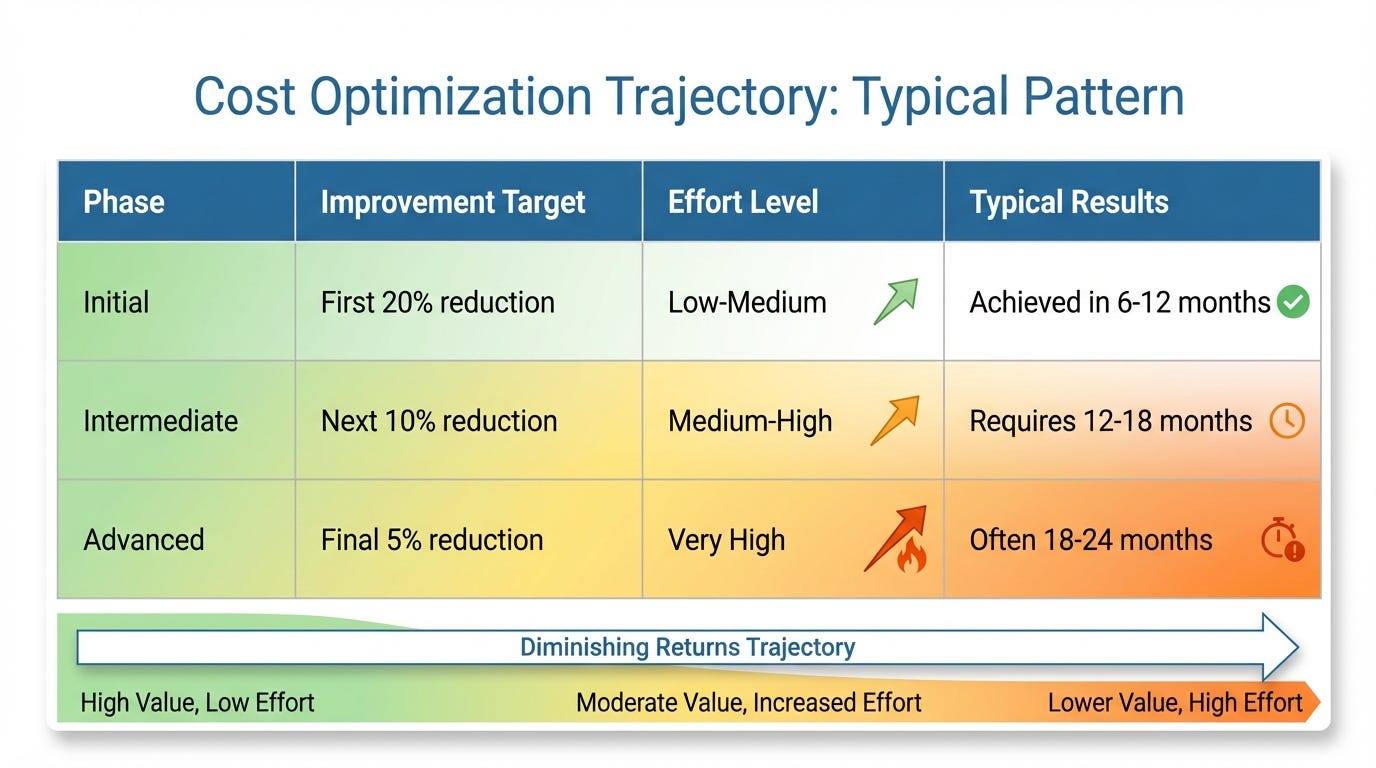

2.4 The Plateau Effect

Within a given technical paradigm, optimization follows a logarithmic curve with diminishing returns.

Typical Cost Optimization Trajectory:

Mathematical Reality:

Each percentage point of cost reduction requires exponentially more effort within the same technical paradigm.

Real Data from Industrial Robot Manufacturer:

A major manufacturer’s experience optimizing a 6-axis robot design:

Year 1: 18% cost reduction (supply chain optimization, design refinement)

Year 2: 7% additional reduction (process improvements, DFM)

Year 3: 3% additional reduction (marginal gains across dozens of components)

Year 4: Plateau—further optimization uneconomical

Breaking the Plateau:

Breakthrough improvements require paradigm shifts, not incremental refinement:

Technology substitution (e.g., visual vs. laser navigation)

Architecture reimagination (e.g., modular vs. integrated design)

Manufacturing revolution (e.g., casting vs. welding)

Cross-industry transfer (e.g., automotive techniques to robotics)

The implication: Companies that rely solely on competitive benchmarking exhaust their optimization potential within 3-4 years. Cross-industry innovation resets the curve.

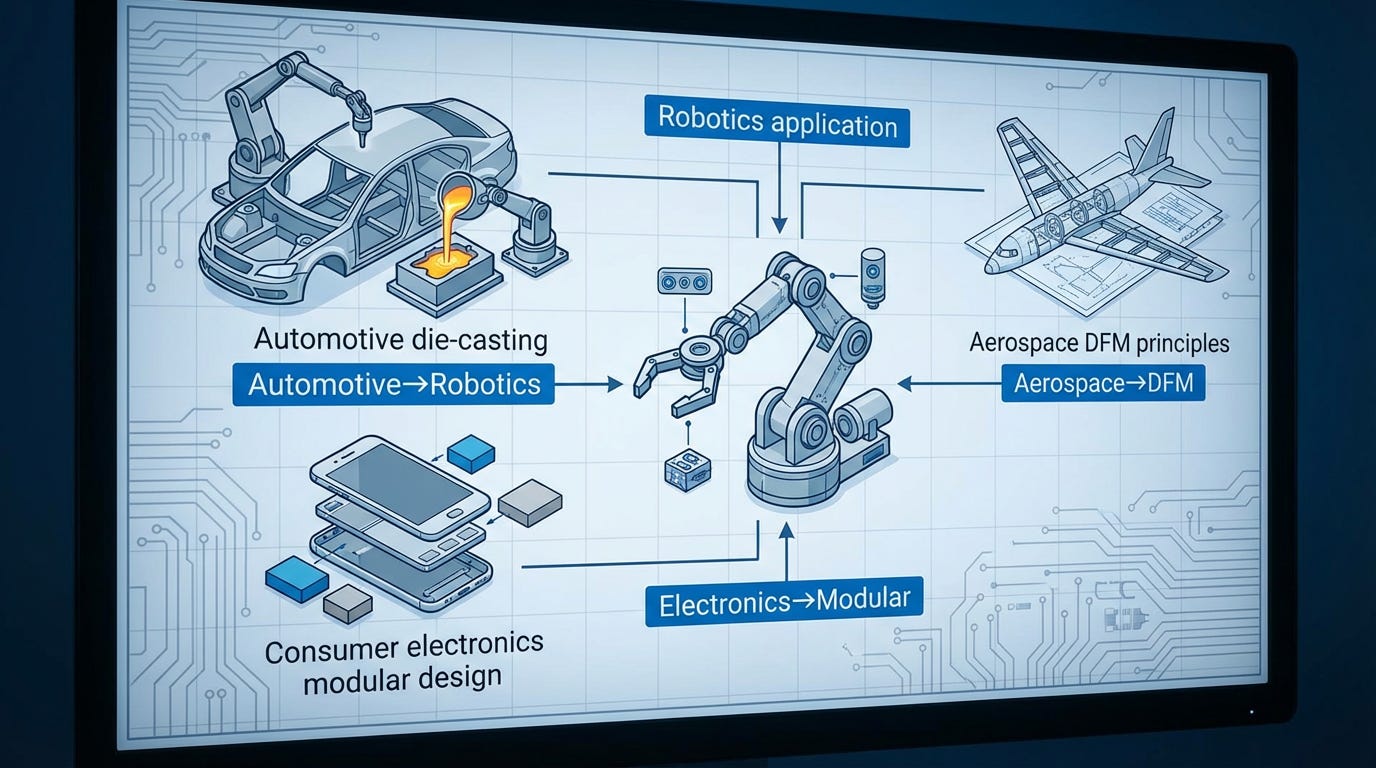

Part III: Cross-Industry Technology Transfer as a Systematic Method

Figure 3: Technology migration pathways from adjacent industries to robotics, showing proven transfer mechanisms

3.1 Automotive Industry: Structural Innovation

The automotive industry’s century-long optimization of high-volume manufacturing provides numerous transferable innovations.

Case Study: Die-Casting Integration

Tesla’s Giga Press technology for automotive structural components inspired direct transfer to robotics manufacturing.

Traditional Robotics Approach:

30+ welded components

12 welding operations

Assembly jigs and fixtures required

High labor content (~8 hours assembly time)

Quality variation from weld inconsistency

Die-Cast Approach (Automotive-Inspired):

Single integrated casting

80% reduction in part count

Eliminated welding operations

Simplified assembly (~2 hours assembly time)

32% cost reduction

Improved structural consistency

Technical Transfer Process:

Feasibility Assessment

Geometry analysis for die-cast compatibility

Material property validation (strength, fatigue)

Tooling investment analysis

Supplier Development

Partner with automotive casting suppliers

Adapt tooling design for robot-scale components

Validate quality systems and process capability

Design Optimization

Rib structure for stiffness

Draft angles for manufacturing

Integrated mounting features

Cable routing provisions

Production Validation

First article inspection

Dimensional capability studies

Load testing and fatigue validation

Cost verification

Results Achieved:

Material cost: -15%

Labor cost: -60%

Cycle time: -75%

Quality escapes: -90%

Total cost impact: -32%

Additional Benefits:

Improved structural rigidity (+18%)

Enhanced consistency (Cpk >1.67)

Reduced quality variation

Faster production ramp capability

Scalability:

This technique scales effectively:

Small robots (<5kg payload): Die-cast aluminum

Medium robots (5-20kg): Die-cast aluminum or magnesium

Large robots (>20kg): Cast iron or steel (selective application)

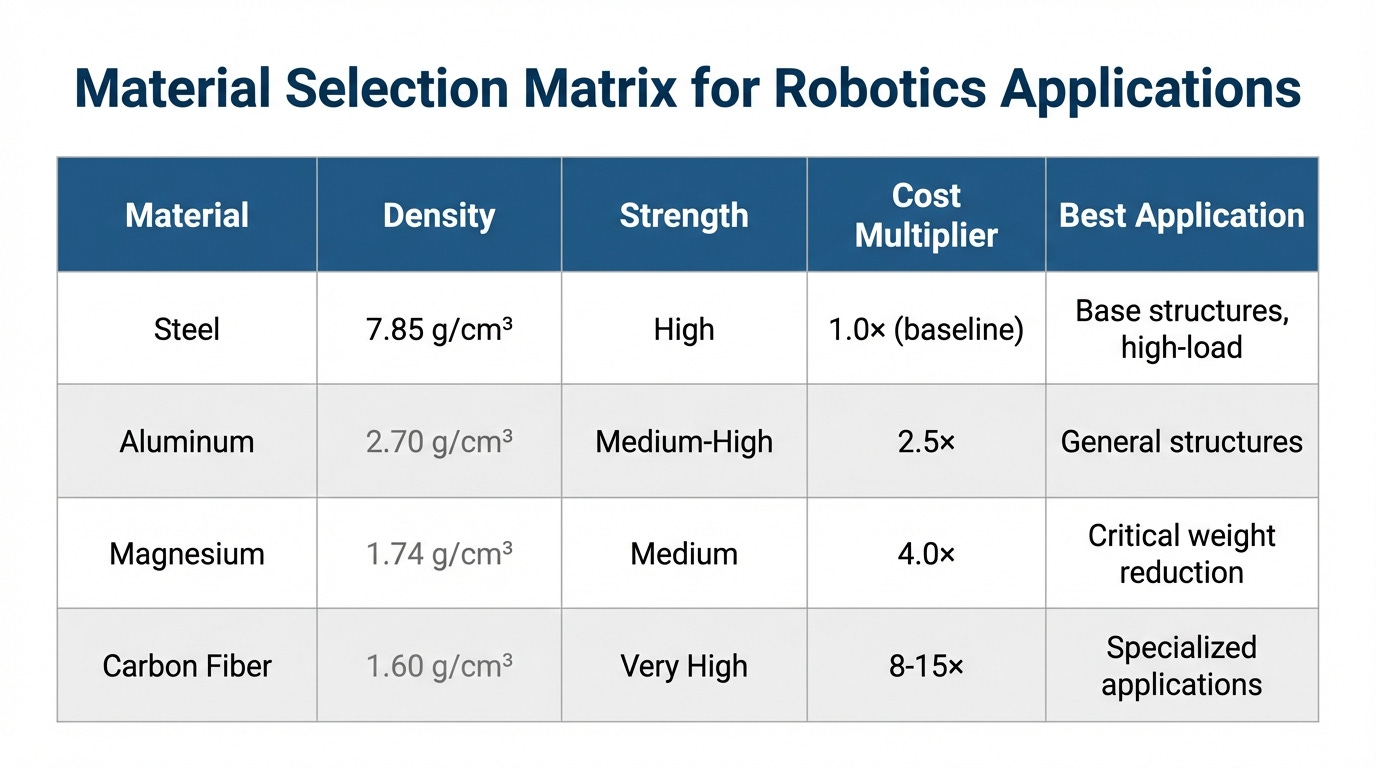

Material Science Transfer: Lightweighting

Automotive lightweighting expertise directly applies to robotics with minimal adaptation:

Material Selection Matrix:

Real Implementation Example:

A collaborative robot manufacturer applied automotive material science:

Component: Robot Arm Links

Original design: Welded steel tube, 3.2kg per link

Optimization 1: Aluminum extrusion, 1.8kg per link (-44%)

Optimization 2: Topology-optimized cast aluminum, 1.4kg per link (-56%)

System Impact:

6-axis robot total weight: 42kg → 25kg

Payload-to-weight ratio: +68%

Energy consumption: -35%

Transport/installation: Easier handling

Economic Analysis:

Material cost increase: +$180 per robot

Reduced motor/gearbox size savings: -$420 per robot

Assembly time savings: -$95 per robot

Net cost reduction: $335 per robot

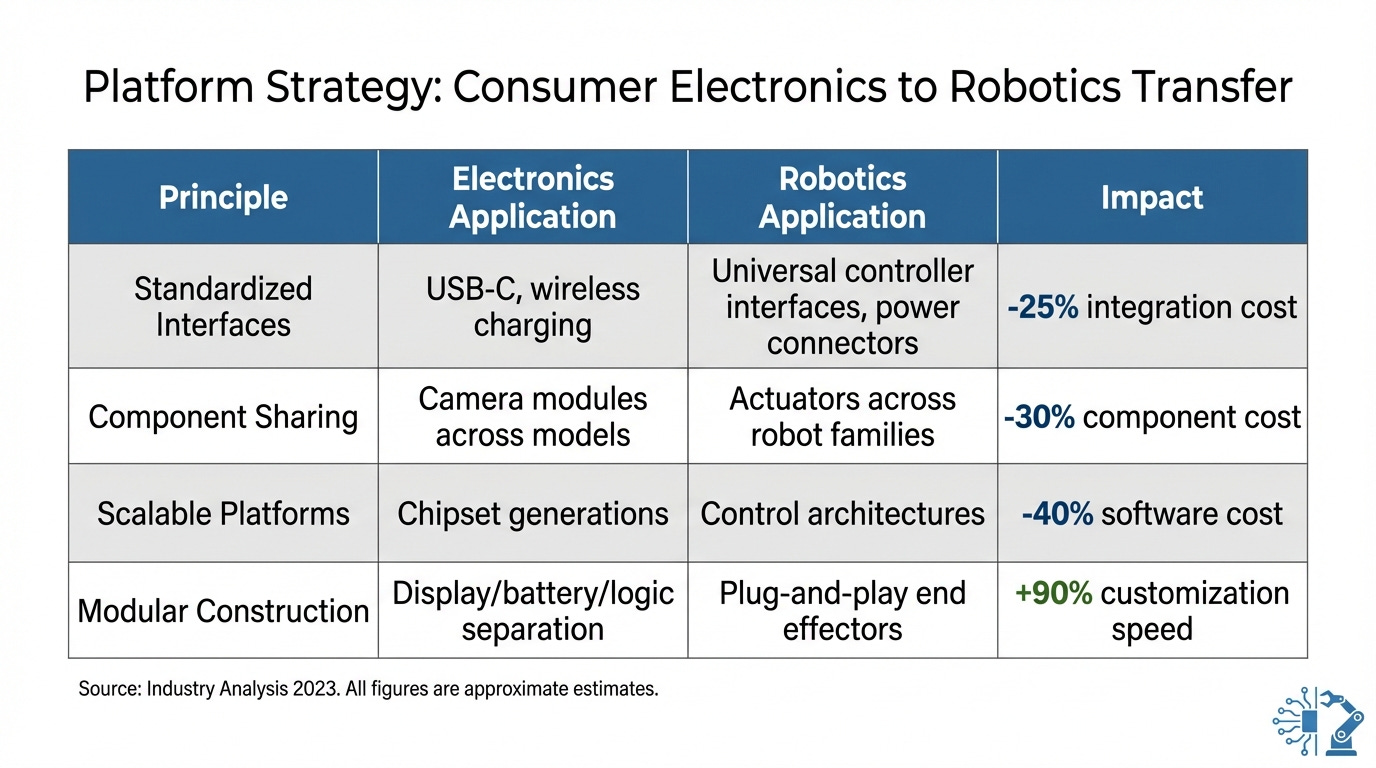

3.2 Consumer Electronics: Modularization

The consumer electronics industry’s mastery of platform strategy and modular architecture offers powerful lessons for robotics.

Platform Strategy from Smartphones:

Impact on Robotics Economics:

A European industrial robot manufacturer implementing electronics-inspired modularity:

Before Modularization:

12 robot models

180 unique part numbers

Average development time: 14 months per model

Inventory carrying cost: 18% of revenue

After Modularization:

12 robot models (same external variety)

85 unique part numbers (-53%)

Average development time: 6 months per model (-57%)

Inventory carrying cost: 9% of revenue (-50%)

Total Cost Impact:

Component procurement: -25% (volume consolidation)

Inventory costs: -50% (fewer SKUs)

Development costs: -60% (platform reuse)

Overall manufacturing cost reduction: 28%

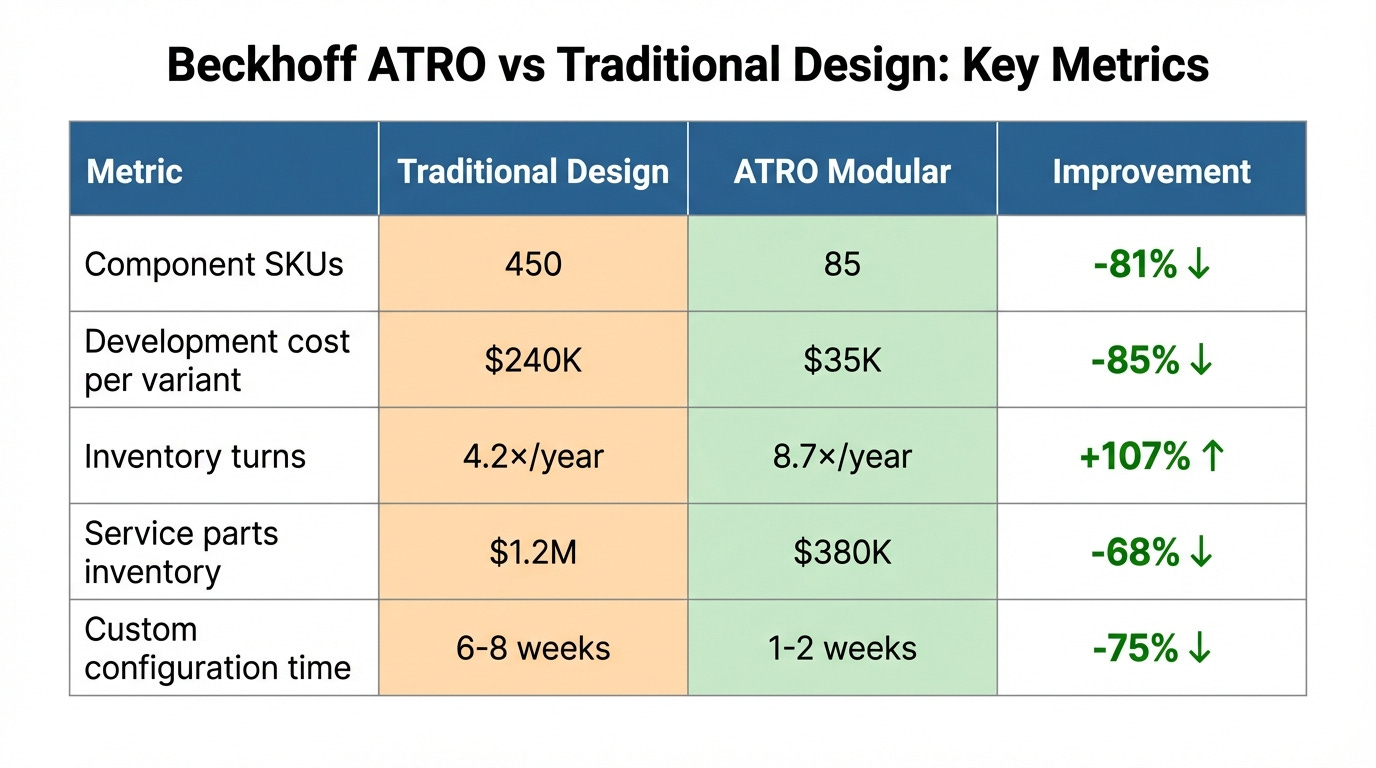

Beckhoff ATRO Modular System: Detailed Analysis

Beckhoff’s ATRO (Automation Technology for Robotics) exemplifies consumer electronics thinking applied to industrial robotics:

Design Principles:

Motor modules: Standardized interface, multiple torque classes

Connection modules: Plug-and-play linking with integrated power/data

Unlimited rotation: All axes support continuous rotation (no cable wrap)

Scalable configurations: 1-10 axes from same component set

Economic Model:

Customer Benefits:

Lower entry cost (standard modules cheaper than custom)

Faster delivery (configure vs. engineer)

Simplified service (standardized spare parts)

Future expandability (add axes without redesign)

Manufacturer Benefits:

Development cost amortized across product line

Higher volume per component (economies of scale)

Simplified inventory management

Faster market response

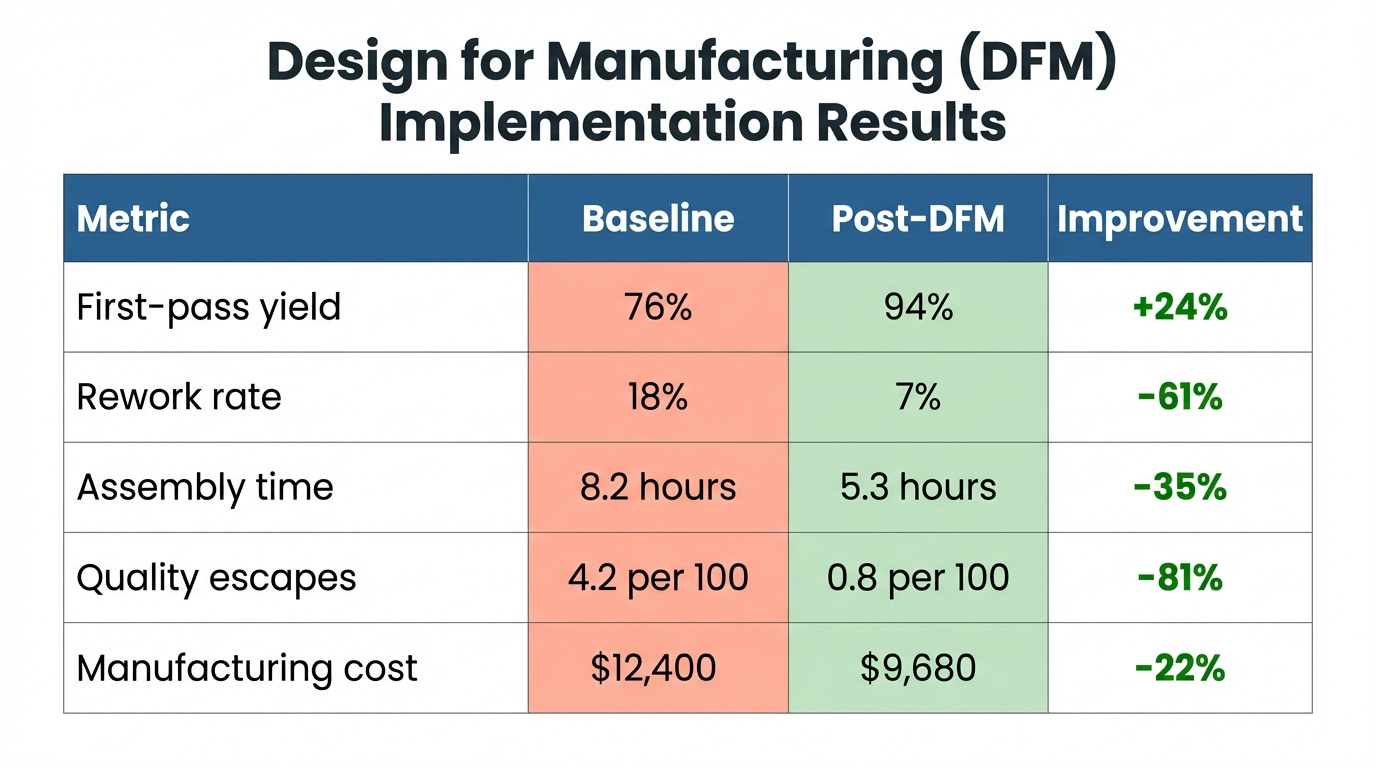

3.3 Aerospace: DFM Excellence

The aerospace industry’s extreme reliability requirements and tight tolerances have created the world’s most sophisticated Design for Manufacturing (DFM) methodologies.

Core DFM Principles from Aerospace:

Design-stage manufacturability analysis

Virtual assembly simulation

Tolerance stack-up analysis

Producibility scoring before prototype

Assembly operation minimization

“Design for Assembly” (DFA) scoring

Part consolidation strategies

Symmetrical design for orientation-insensitive assembly

First-pass yield optimization

Process capability indices (Cpk) requirements

Poka-yoke (error-proofing) integration

Statistical process control from day one

Process capability integration

Design tolerances matched to process capability

Critical characteristics identified and controlled

Supplier process audits before design freeze

Transfer to Robotics: Case Study

An Asian electronics manufacturer producing inspection robots adopted aerospace DFM principles:

Implementation Timeline:

Phase 1 (Months 1-3): Assessment & Training

Baseline process capability study

Engineering team training (40 hours)

DFM software tools implementation

Phase 2 (Months 4-9): Pilot Project

Redesign of 5-axis inspection robot

DFM principles applied to 120 components

Virtual assembly and tolerance analysis

Phase 3 (Months 10-12): Production Validation

First article inspection (15 units)

Process capability verification

Documentation and standard work

Results:

Key DFM Interventions:

Part Count Reduction

Original: 127 unique parts

Optimized: 89 unique parts (-30%)

Method: Multi-function part design, consolidation

Tolerance Rationalization

40% of tolerances tighter than necessary

Relaxed non-critical tolerances by 1-2 classes

Manufacturing cost reduction: 12%

Assembly Sequence Optimization

Eliminated 15 “flip/rotate” operations

Introduced modular sub-assemblies

Parallel assembly paths enabled

Error-Proofing (Poka-Yoke)

Asymmetric connectors (prevent mis-insertion)

Mechanical interlocks for assembly sequence

Visual alignment features

Sustainability Impact:

DFM also improves environmental metrics:

Scrap reduction: 18% less material waste

Rework energy: 60% reduction

Packaging optimization: 25% smaller footprint

3.4 Navigation Technology: Autonomous Vehicle Crossover

Mobile robot navigation directly benefits from the multi-billion dollar R&D investments in autonomous vehicles.

Technology Evolution:

Autonomous Vehicle Technology Spillover:

The AV industry’s massive investment creates robotics benefits:

Investment Scale:

Waymo: >$5 billion (2009-2024)

Cruise: >$10 billion

Tesla Autopilot: >$3 billion

Chinese AV companies: >$15 billion combined

Robotics Benefit Mechanisms:

Sensor Cost Reduction

LIDAR: $75,000 (2010) → $500 (2025)

HD cameras: $2,000 (2015) → $150 (2025)

IMU sensors: $5,000 (2010) → $50 (2025)

Algorithm Open-Sourcing

ORB-SLAM (Oxford)

Cartographer (Google)

RTAB-Map (Université de Sherbrooke)

Computing Platform Maturation

NVIDIA Jetson: $1,000, 5 TOPS (2015)

NVIDIA Orin: $500, 200 TOPS (2024)

40× performance, 50% cost reduction

Commercial Impact Analysis:

Case: Commercial Cleaning Robot Evolution

Market Penetration Effect:

The cost reduction unlocked new market segments:

2018: 12,000 units deployed globally (mostly airports, hospitals)

2024: 180,000 units deployed globally (+1,400%)

New segments enabled: Retail stores, office buildings, schools, restaurants

Technology Roadmap:

The next wave combines multiple technologies:

Visual-Inertial Odometry: Drift-free localization

3D semantic understanding: Object recognition + navigation

Multi-floor mapping: Elevator integration

Cloud fleet learning: Shared map improvements

Regional Market Dynamics:

Technology adoption varies by cost sensitivity:

Key Insight: AV investment created a “rising tide” that lifted all boats—robotics companies globally benefit regardless of their own R&D budgets.

Part IV: The Three-Dimensional Cost Reduction Framework

Effective cost reduction operates across three dimensions simultaneously, not sequentially. Most organizations optimize in only one or two dimensions, leaving significant value uncaptured.

4.1 Strategic Dimension (Altitude): Cost-Value Balance

The Fundamental Question: What costs are essential to value delivery, and which are not?

Cost reduction must preserve or enhance value delivery. Indiscriminate cutting destroys competitive positioning.

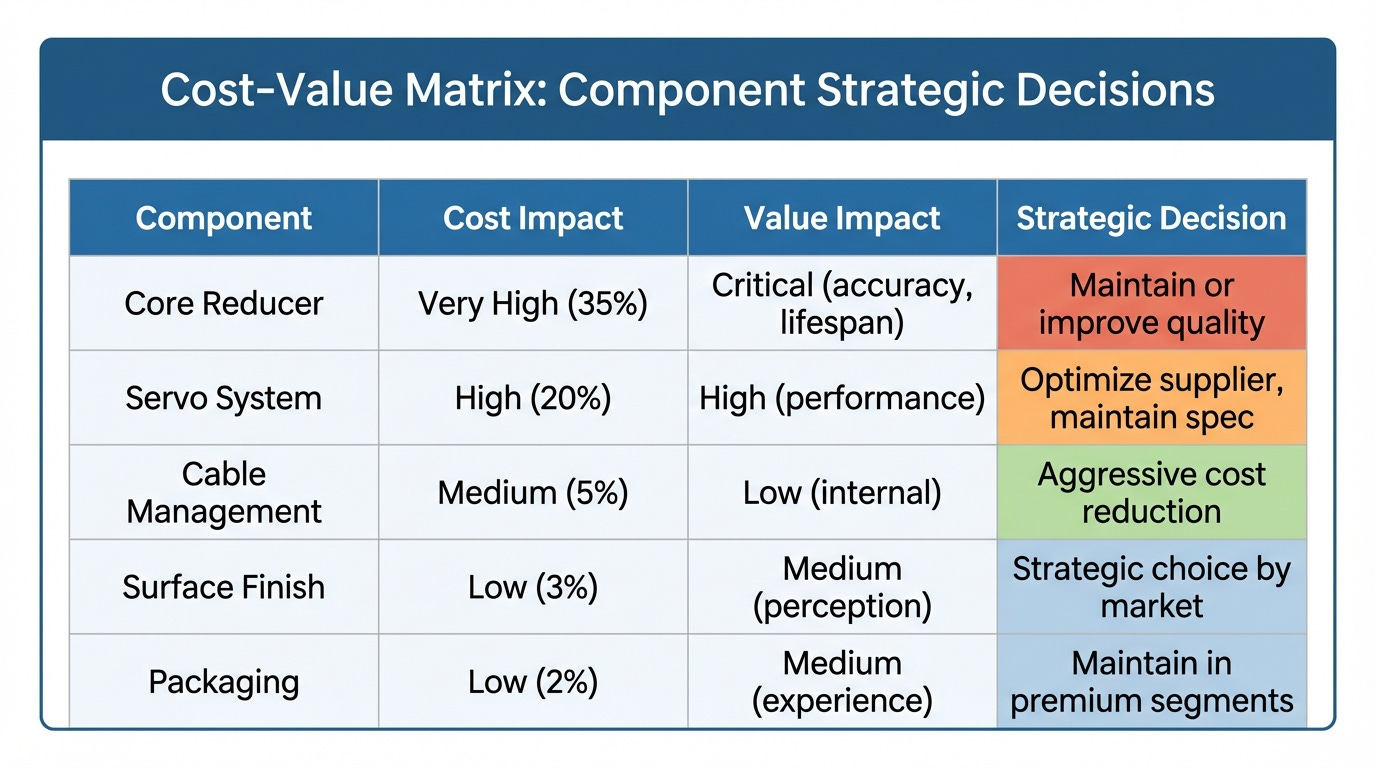

Framework: Cost-Value Matrix

Real Example: Collaborative Robot De-Contenting Decision

A manufacturer analyzed 80 design elements across cost and value dimensions:

High-Value, High-Cost (Maintain):

Force/torque sensing system

Motor quality and control

Safety systems

High-Value, Lower-Cost (Protect):

Cable routing aesthetics

LED status indicators

Emergency stop accessibility

Low-Value, High-Cost (Reduce):

Over-specified connectors (industrial → commercial grade)

Unnecessary machining tolerances (relaxed 40% of specs)

Redundant documentation (streamlined)

Low-Value, Low-Cost (Maintain):

Brand badging

Color customization

Basic cable management

Results:

Total cost reduction: 18%

Customer satisfaction: Unchanged (95th percentile maintained)

Premium positioning: Preserved

The Lesson: Strategic cost reduction requires intimate understanding of what customers value versus what engineers traditionally specify.

4.2 Technical Dimension (Depth): Engineering Optimization

Systematic Engineering Cost Reduction Methods:

1. Topology Optimization

Mathematical optimization of material distribution for strength-to-weight ratio.

Example Application: Robot Link

Original design: Uniform wall thickness, 2.8kg

Topology optimized: Variable thickness, strategic ribbing, 1.7kg (-39%)

Structural performance: +5% stiffness

Cost impact: -$45 per link (material + machining time)

Tools: Ansys, Altair OptiStruct, Autodesk Fusion 360

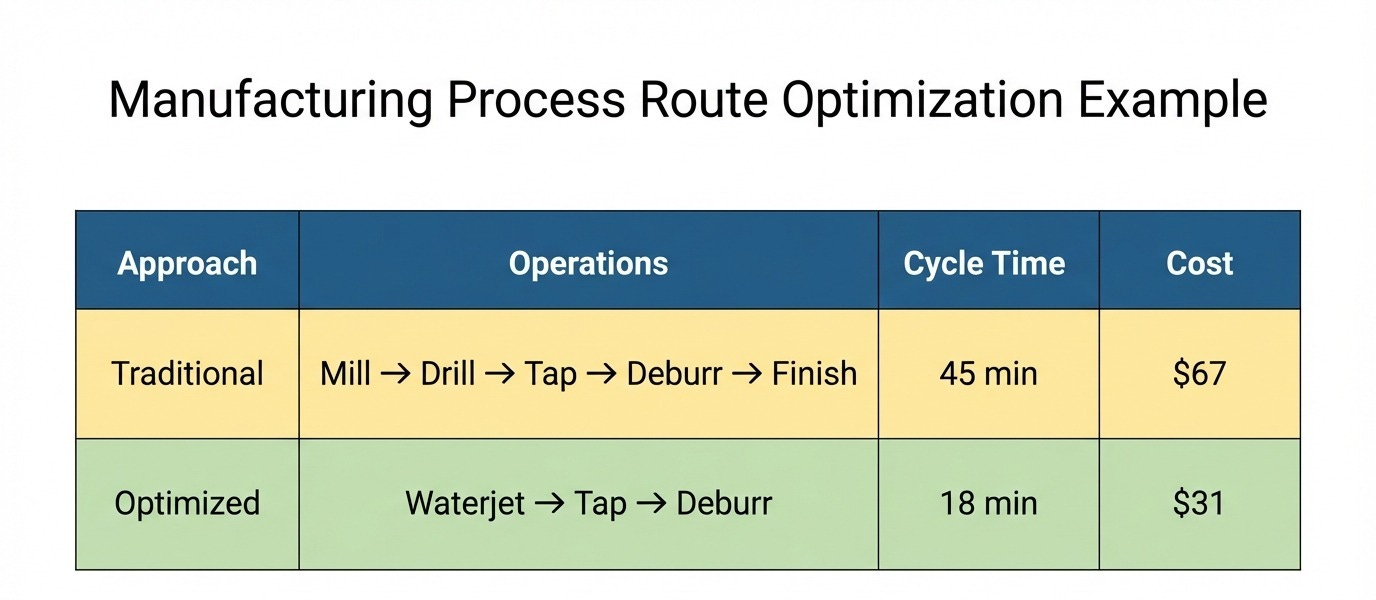

2. Process Route Optimization

Reducing manufacturing operations through design changes.

Example: Base Plate Manufacturing

Design changes enabling optimization:

Relaxed tolerances on non-critical features

Eliminated pockets requiring milling

Standardized hole patterns

3. Material Substitution

Performance-equivalent materials at lower cost.

Case Study: Actuator Housing

Original: 6061-T6 aluminum, machined

Alternative: A380 aluminum, die-cast

Performance: Equivalent strength, slightly lower machinability

Cost: -45% (-$28 per unit)

Volume threshold: 1,000+ units for tooling ROI

4. Supply Chain Localization

Developing regional suppliers reduces logistics and diversifies risk.

Example: Asian Robot Manufacturer Entering North America

Initial (Imported):

Component sourcing: 95% from Asia

Lead time: 8-12 weeks

Logistics cost: 12% of landed cost

Supply risk: High (single-region dependency)

Localized (3 years later):

Component sourcing: 60% North American

Lead time: 2-4 weeks

Logistics cost: 4% of landed cost

Supply risk: Diversified

Total cost impact: -15% (despite higher component costs)

4.3 Cognitive Dimension (Breadth): The Innovation Multiplier ⭐

This often-neglected dimension delivers disproportionate returns because it operates outside the constraints of your current paradigm.

Why Cognitive Breadth Matters:

Engineers trained in robotics naturally reference robotic solutions. This creates convergent thinking within industry norms.

Cognitive diversity—exposure to solutions from other industries—breaks this pattern.

Systematic Approach to Cross-Industry Intelligence:

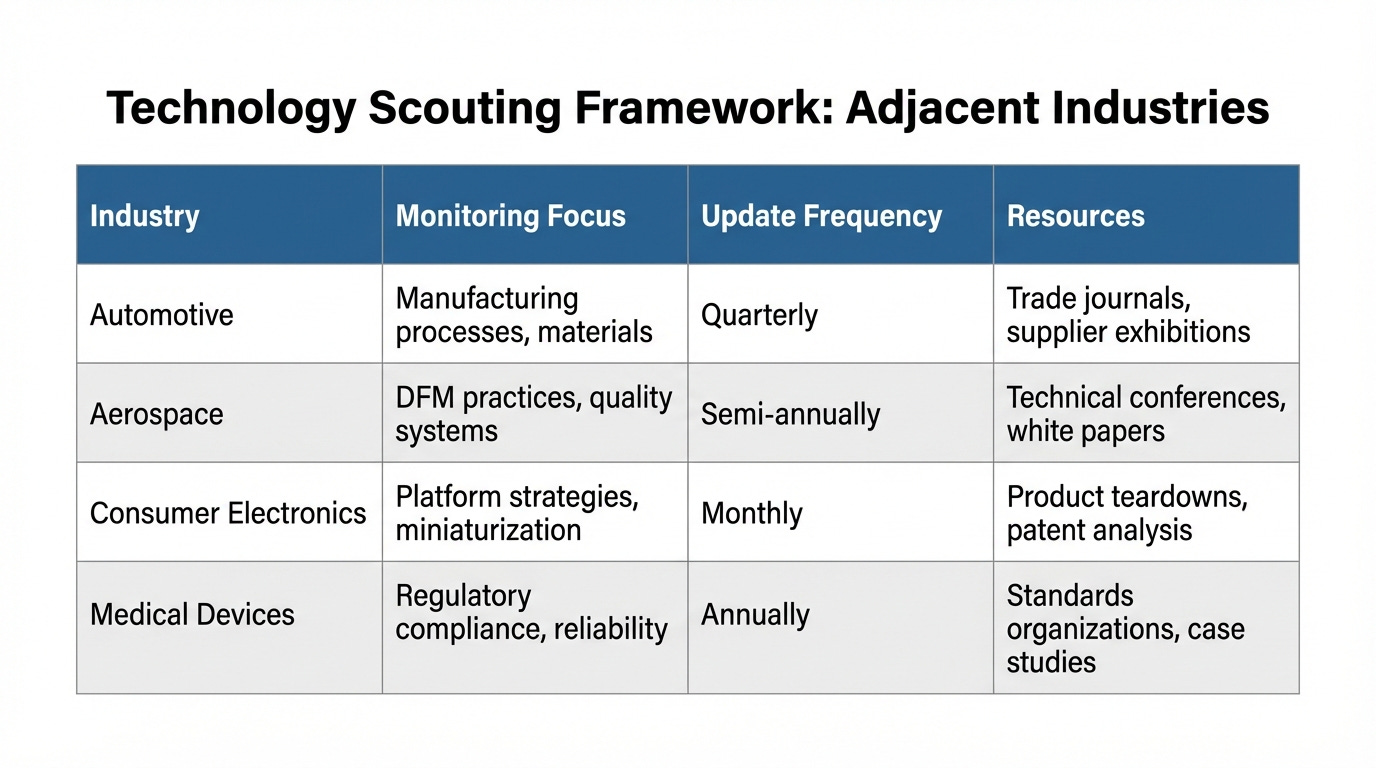

1. Technology Scouting Framework

Establish structured monitoring of adjacent industries:

2. Patent Landscape Analysis

Patents reveal technology directions 3-5 years before market adoption:

Example Analysis:

Search: “Lightweight actuator” in automotive sector (2019-2024)

Finding: 40% increase in magnesium alloy applications

Insight: Material science maturing, suppliers scaling capacity

Action: Robotics team evaluates magnesium for 2026 product line

Result: 28% weight reduction, 18% cost increase, net value positive

3. Supplier Cross-Pollination

Your suppliers work across industries and possess transferable knowledge:

Best Practice:

Quarterly supplier technology reviews

Question: “What innovations are you implementing for other industries?”

Document insights in technology database

Assign engineering team to evaluate applicability

Example:

Casting supplier mentions automotive lightweighting project using hybrid foam-core casting

Robotics team investigates application to robot base structure

Pilot program reveals 35% weight reduction + 18% cost reduction

Full implementation in 18 months

4. Cross-Functional Job Rotation

Engineers with multi-industry experience bring cognitive diversity:

Program Structure:

6-12 month rotations to adjacent industries (automotive, aerospace partnerships)

Structured learning objectives

Knowledge transfer upon return

Documented best practices

Results from European Manufacturer:

15 engineers completed rotations over 3 years

23 significant process improvements attributed to rotation program

Estimated value: $2.8M in cost reductions and improvements

Cultural shift toward cross-industry learning

Organizational Implementation:

Team Level:

Quarterly Cross-Industry Forums: 2-hour sessions reviewing adjacent industry trends

Innovation Budget: 5% of R&D for exploring non-obvious solutions

Failure Tolerance: Explicitly permit failed experiments from cross-industry exploration

Individual Level:

Expanded Technical Reading: 20% time allocated to non-robotics technical content

Conference Diversity: Attend 1 non-robotics conference per year

Patent Review: Monthly review of cross-industry patent applications

Project Level:

Mandatory Cross-Industry Reference: Every design review must include 2+ non-robotics precedents

“Why Not?” Analysis: Question industry assumptions explicitly

Alternative Costing: Estimate cost of solutions from other industries before defaulting to robotics norms

Cultural Level:

Celebrate Paradigm-Shifting Ideas: Recognize proposals that challenge conventions

Failure Retrospectives: Document valuable lessons from unsuccessful cross-industry transfers

Knowledge Sharing: Internal wiki documenting cross-industry insights

Part V: Implementation Roadmap

5.1 Organizational Capabilities: Building the Foundation

Phase 1: Assessment (Months 1-3)

Current State Analysis:

Map existing cost structure with granular detail

Benchmark against competitive products

Identify cognitive biases in team (”we’ve always done it this way”)

Survey adjacent industries for relevant innovations

Assess IP landscape for constraints and opportunities

Deliverables:

Cost waterfall diagram showing component-level breakdown

Competitive benchmarking report (know your baseline)

Cross-industry opportunity matrix

IP freedom-to-operate analysis

Prioritized improvement opportunities

Phase 2: Capability Building (Months 4-9)

Cross-Industry Awareness:

Subscribe to trade publications from automotive, aerospace, electronics

Attend cross-industry conferences (SAE, AIAA, IEEE)

Establish relationships with suppliers serving multiple industries

Create cross-industry patent monitoring alerts

Develop technology scouting framework

Training Programs:

DFM/DFA training (40 hours, certification optional)

Topology optimization tools (Ansys, Altair)

Cost modeling and analysis

IP landscape navigation

Cross-industry case study workshops

Tools & Systems:

Implement cost modeling software

Create innovation database (cross-industry insights)

Establish design review checklists (cross-industry references mandatory)

Develop supplier technology questionnaire

Phase 3: Pilot Projects (Months 10-18)

Project Selection Criteria:

Medium cost impact ($100K-$500K annual savings potential)

Limited scope (single subsystem)

Measurable outcomes

Acceptable failure risk

Example Pilot Projects:

Pilot A: Automotive Casting Transfer

Objective: Replace welded frame with cast structure

Timeline: 12 months

Investment: $180K (tooling + engineering)

Success criteria: 20% cost reduction, equivalent performance

Pilot B: Electronics Modularization

Objective: Platform strategy for controller architecture

Timeline: 15 months

Investment: $240K (redesign + validation)

Success criteria: 30% SKU reduction, 15% cost reduction

Pilot C: Aerospace DFM Application

Objective: Reduce assembly operations by 40%

Timeline: 9 months

Investment: $95K (design optimization + tooling changes)

Success criteria: 25% assembly time reduction

Documentation:

Detailed project plans with milestones

Risk registers and mitigation strategies

Regular steering committee reviews

Comprehensive retrospectives

Phase 4: Scaled Implementation (Months 19-36)

Rollout Strategy:

Based on pilot results:

Success: Scale to similar applications across product line

Partial success: Refine methodology, second-generation pilot

Failure: Document lessons, pivot approach

Organizational Integration:

Formal design review gates with cross-industry requirements

Cost reduction targets allocated across three dimensions

Innovation metrics tracked at team and individual level

Supplier collaboration program established

Knowledge management system populated

Continuous Improvement:

Quarterly reviews of cross-industry landscape

Annual benchmarking against competitive cost structures

Systematic capture of emerging technologies

Regular training refreshers and capability updates

5.2 Individual Mindset: Engineering Team Development

Cultivating Cross-Industry Thinking:

Monthly Practices:

Technical Paper Review: Each engineer presents one non-robotics paper

Patent Analysis: Review 5 patents from adjacent industries

Product Teardown: Analyze consumer or automotive product with cost focus

Quarterly Practices:

Industry Immersion: Visit automotive plant, electronics manufacturer, or aerospace facility

Supplier Technology Day: Deep dive with key suppliers on their innovation roadmap

Scenario Planning: “What if we applied X industry’s approach to our Y problem?”

Annual Practices:

Cross-Industry Conference: Each engineer attends one non-robotics conference

Rotation Program: 1-2 engineers on temporary assignment to adjacent industry

Innovation Summit: Full team workshop exploring paradigm-shifting ideas

Incentive Alignment:

Performance reviews include “cognitive breadth” dimension

Innovation awards for cross-industry transfer ideas

Publication encouragement in cross-industry forums

Career development paths reward diverse experience

5.3 Project Execution: Practical Framework

Stage 1: Opportunity Identification

Activities:

Detailed cost structure mapping

Value analysis (customer priorities vs. cost drivers)

Cross-industry technology scan

IP landscape review

Supplier capability assessment

Outputs:

Prioritized opportunity list

Technology transfer feasibility assessments

Preliminary ROI estimates

Risk identification

Go/No-Go Criteria:

Minimum $100K annual savings potential

Technical feasibility >70% confidence

IP freedom-to-operate confirmed

Supplier support committed

Stage 2: Feasibility Deep Dive

Technical Analysis:

Performance modeling and simulation

Material compatibility verification

Manufacturing process validation

Quality system implications

Regulatory compliance check

Economic Analysis:

Detailed cost modeling (material, labor, tooling, overhead)

Investment requirements (NRE, capital equipment)

Volume sensitivity analysis

NPV and IRR calculation

Payback period assessment

Risk Analysis:

Technical risks (performance, reliability)

Supply chain risks (supplier capability, capacity)

Market risks (customer acceptance, competitive response)

IP risks (patent infringement, design-around costs)

Outputs:

Detailed business case

Risk mitigation plan

Project plan with milestones

Resource requirements

Stage 3: Pilot Implementation

Execution:

Design iteration with cross-functional team

Prototype development and testing

Supplier qualification and validation

Cost verification (actual vs. modeled)

Performance validation

Validation:

First article inspection

Reliability testing (accelerated life)

Customer beta program (if applicable)

Manufacturing process capability study

Quality system documentation

Decision Point:

Proceed to production: Clear success, meet all criteria

Iteration required: Promising but needs refinement

Terminate: Fundamentally flawed, pivot to alternative

Stage 4: Production Scale-Up

Launch Preparation:

Manufacturing process documentation

Supply chain activation (capacity, contracts)

Quality control plan implementation

Training (assembly, inspection, maintenance)

Launch readiness review

Ramp Management:

Controlled production ramp (50 → 200 → 1000+ units)

Closely monitored quality metrics

Cost tracking vs. model

Customer feedback loop

Continuous improvement actions

Sustaining Phase:

Ongoing cost optimization

Supplier performance management

Design refinement based on field data

Lessons learned documentation

Technology transfer to other product lines

Conclusion: From Cost Follower to Innovation Leader

The robotics industry stands at an inflection point. Cost pressures intensify as the market expands and matures, while technical possibilities multiply through advances in AI, materials science, and manufacturing technologies. Success in this environment requires transcending the limitations of competitive benchmarking.

Key Insights Recap:

1. Competitive Benchmarking’s Inherent Limitations

Creates followers, not innovators

Provides solutions without problem-solving context

Leads to industry homogenization

Produces diminishing returns within paradigms

Cannot break through cost plateaus

2. Cross-Industry Transfer as Systematic Methodology

Unlocks non-linear cost reductions (25-40% vs. 5-10%)

Provides patent-free design inspiration

Breaks cognitive lock-in patterns

Resets optimization curves

Creates differentiated market positioning

3. Three-Dimensional Framework Necessity

Strategic (Altitude): Cost-value balance preservation

Technical (Depth): Engineering optimization rigor

Cognitive (Breadth): Cross-industry intelligence—the force multiplier

4. Implementation as Organizational Capability

Not occasional insight, but systematic process

Requires investment in awareness, tools, culture

Builds compounding competitive advantage

Creates sustainable cost leadership

The Path Forward: Practical Next Steps

For Engineering Teams:

This Month: Subscribe to one automotive and one aerospace publication

This Quarter: Attend one cross-industry conference or facility tour

This Year: Pilot one cross-industry technology transfer project

Long-term: Build systematic cross-industry monitoring capability

For Engineering Managers:

Immediate: Add cross-industry reference requirement to design reviews

Near-term: Allocate 5% R&D budget to exploratory cross-industry projects

Medium-term: Establish technology scouting and patent monitoring process

Strategic: Develop cross-industry rotation program for key engineers

For Executives:

Strategic: Commission cross-industry opportunity assessment

Organizational: Measure and reward cognitive breadth in performance systems

Investment: Fund DFM training and cross-industry exploration

Cultural: Celebrate paradigm-shifting ideas, even failed experiments

The Compounding Advantage

Organizations that master cross-industry technology transfer gain advantages that compound over time:

Year 1 Benefits:

Identification of non-obvious cost reduction opportunities

Avoidance of competitor patent minefields

Fresh perspective on industry assumptions

Year 3 Benefits:

Systematic cost advantage across product line

Differentiated technical capabilities

Supplier relationships across industries

Organizational learning culture

Year 5+ Benefits:

Industry leadership in cost position

Innovation reputation attracting talent

Platform advantages (modular, scalable architectures)

Sustainable competitive moat

Final Reflection

True cost reduction doesn’t come from copying what others do—it comes from understanding why others can do it, and transferring those fundamental principles to create your own systematic solutions.

The boundary of cost reduction is redefined not by industry norms, but by cognitive breadth and systematic execution.

When you evolve from competitive benchmarking to cross-industry technology transfer, you transform from a cost follower to an innovation leader. Your cost structure becomes a strategic advantage, not just an operational metric.

The robotics companies that thrive in the next decade will be those that look beyond their industry for inspiration, systematically transfer innovations from adjacent fields, and build organizational capabilities for continuous paradigm-shifting thinking.

The question is not whether to adopt cross-industry thinking, but how quickly you can build this capability before your competitors do.

About This Analysis

This analysis draws on technical and economic research across the global robotics industry, examining cost structures, manufacturing innovations, and technology transfer patterns from automotive, aerospace, and consumer electronics sectors. The frameworks presented have been validated through implementations at industrial, collaborative, mobile, and humanoid robot manufacturers across North America, Europe, and Asia.

The case studies represent real implementations with details modified for confidentiality where appropriate. All cost figures and percentage improvements are based on documented industry data or direct manufacturer reporting.

Further Reading & Resources

Cross-Industry Technology Transfer:

“Innovation from Adjacent Industries: A Framework” - MIT Sloan Management Review

“The Medici Effect: Breakthrough Insights at the Intersection of Ideas” - Frans Johansson

“Design for Manufacturability Handbook” - McGraw-Hill Professional

Robotics Cost Engineering:

“Cost structure evolution in humanoid robotics” - IEEE Robotics & Automation Magazine

“Supply chain strategies for component localization” - International Journal of Production Economics

“DFM implementation frameworks for robotics” - Journal of Manufacturing Systems

Industry Reports:

International Federation of Robotics: World Robotics Report (Annual)

ARK Invest: Big Ideas Report (Annual) - Robotics section

McKinsey: “The Future of Manufacturing” reports

Technology Scouting:

Google Patent Search - Set up alerts for adjacent industry innovations

TechCrunch, IEEE Spectrum - Cross-industry technology news

SAE International, AIAA - Technical paper databases

🎯 Master Robotics Engineering (The Way School Never Taught)

After 13 years in the field, I’ve learned that the best engineering knowledge doesn’t come from textbooks—it comes from real projects, failures, and breakthroughs.

That’s what I share every week in The Robotics Engineer’s Digest:

Technical Deep Dives → Real engineering analysis with formulas

Case Study Breakdowns → Learn from $100K+ mistakes (so you don’t repeat them)

Component Selection Guides → Decision frameworks for motors, reducers, sensors

Industry Intelligence → What’s actually happening in humanoid robotics, automation, AI

100% free. Zero spam. Unsubscribe anytime.

💬 What Are You Working On Right Now?

I create content based on what engineers actually need.

Comment below and tell me:

What type of robot/automation project are you working on?

What’s your biggest technical challenge right now?

What topic would you like me to cover next?

100+ engineers have already shared. Your input shapes future articles!

Join 100+ robotics engineers getting smarter every week:

Couldn't agree more, this insight on moving beyond competitive benchmarking is spot on. It makes me think of your earlier work exploring systemic shifts in technology development. I wonder if this 'cost reduction parodox' is something we see in AI model training too, where everyone tries to beat the same benchmark?